Table of Contents

- What Happens If You Own Multiple Life Insurance Policies?

- Is It Legal to Have More Than One Life Insurance Policy?

- Why People Buy Multiple Life Insurance Policies

- The Biggest Benefits of Multiple Policies

- Real-Life Examples

- The Life Insurance Laddering Strategy

- Potential Downsides to Consider

- How Much Coverage Is Too Much?

- Frequently Asked Questions

- Final Thoughts

What Happens If You Own Multiple Life Insurance Policies?

Most people believe life insurance is a one-time purchase. You buy a policy, pay your premiums, and your family receives financial protection if something happens to you.

In reality, many people own several life insurance policies at the same time.

A person may have coverage through their employer, a personal term life insurance policy, and a permanent life insurance policy designed for long-term financial planning. These policies can work together to provide broader protection than a single policy alone.

The key is that each policy serves a specific purpose. One may protect your mortgage, another may replace lost income for your family, while another helps with estate planning or wealth transfer.

Is It Legal to Have More Than One Life Insurance Policy?

Yes, absolutely.

There is no law that limits the number of life insurance policies you can own. Insurance companies simply want to ensure the total amount of coverage makes financial sense based on your income, assets, debts, and overall financial situation.

When applying for new coverage, insurers will usually ask about any existing life insurance policies you already have. This helps them assess risk and determine appropriate coverage levels.

As long as you provide accurate information during the application process, owning multiple policies is perfectly legal.

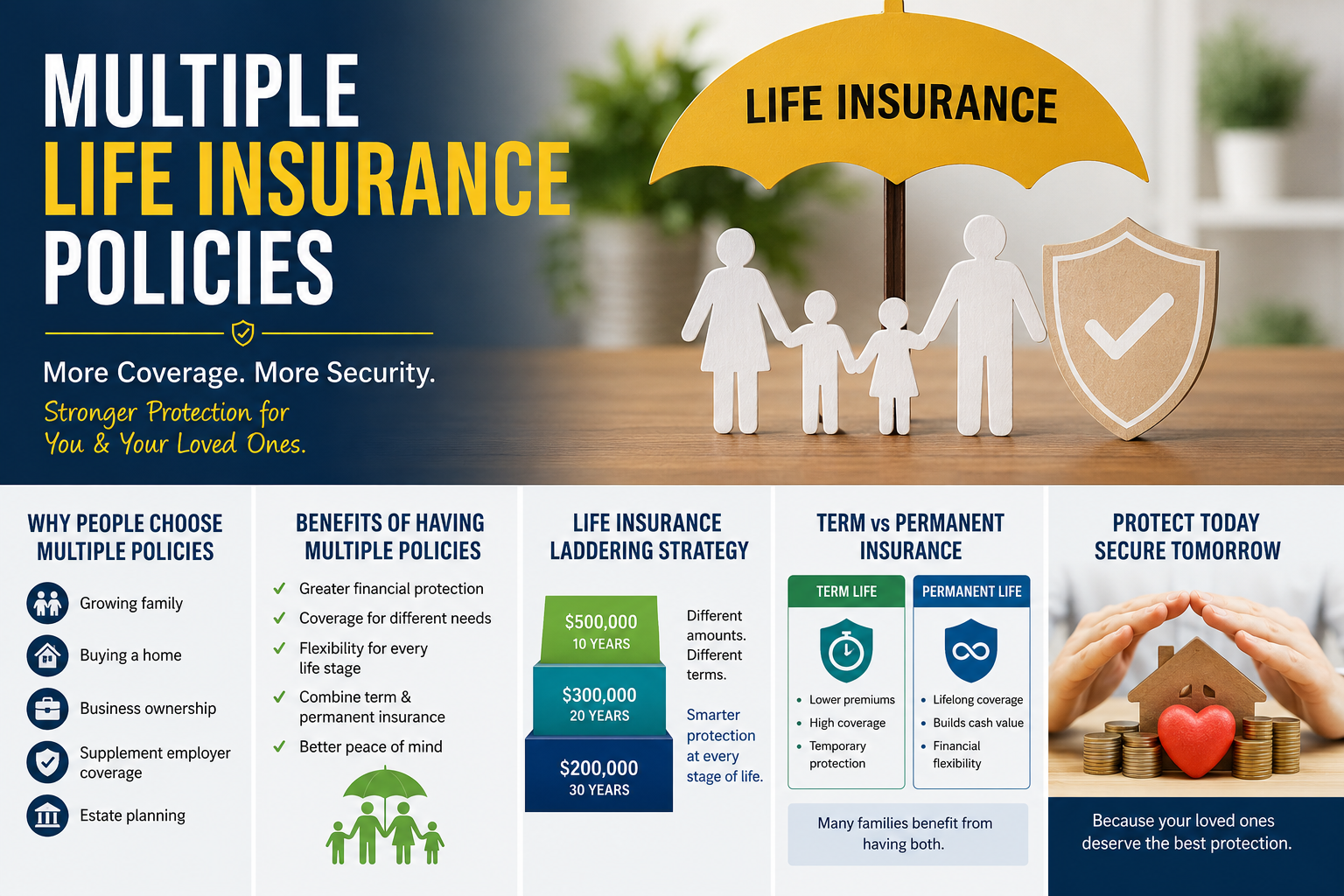

Why People Buy Multiple Life Insurance Policies

Life changes quickly.

The amount of insurance you needed at age 25 is often very different from what you need at age 40.

Here are some common reasons people add additional policies over time:

Starting a Family

When children enter the picture, financial responsibilities increase significantly. Many parents purchase extra coverage to ensure future education costs and daily living expenses are protected.

Buying a Home

A mortgage can become one of the largest financial obligations a family has. Additional life insurance can help ensure loved ones won’t struggle with housing costs if the unexpected happens.

Changing Careers

Employer-provided life insurance is often limited. If you change jobs or lose employment, that coverage may disappear. A personal policy can fill the gap.

Business Ownership

Business owners frequently purchase separate policies to protect business interests while maintaining personal family protection.

Estate Planning

Higher-net-worth individuals often use permanent life insurance as part of broader wealth preservation and inheritance planning strategies.

The Biggest Benefits of Multiple Policies

1. Greater Financial Security

Different policies can cover different responsibilities.

Instead of relying on a single large policy, you can create layers of protection that address specific needs.

2. More Flexibility

Your financial obligations won’t stay the same forever.

For example, your children will eventually become financially independent, and your mortgage will eventually be paid off. Multiple policies allow your coverage to evolve alongside your life.

3. Potential Cost Savings

Buying several smaller policies with different terms can sometimes cost less than purchasing one massive policy that lasts for decades.

4. Combining Temporary and Permanent Coverage

Many financial planners recommend combining term life insurance with permanent life insurance.

Term insurance provides affordable protection during your highest-risk financial years, while permanent insurance can provide lifelong benefits and potential cash-value growth.

5. Extra Peace of Mind

Knowing that multiple aspects of your financial life are protected often provides families with greater confidence and security.

Real-Life Examples

Example 1: Young Parents

A couple with two children purchases:

- $1,000,000 20-year term policy

- $250,000 whole life policy

The term policy protects the family during the years when the children are financially dependent, while the whole life policy provides lifelong protection.

Example 2: Homeowner

A homeowner may keep an existing life insurance policy and purchase an additional policy specifically designed to cover the remaining mortgage balance.

Example 3: Business Owner

A business owner might maintain:

- Personal family protection coverage

- Key-person insurance

- Business succession insurance

Each policy serves a unique purpose.

The Life Insurance Laddering Strategy

One of the smartest approaches to multiple life insurance policies is known as life insurance laddering.

Instead of purchasing one large policy, you buy several policies with different coverage amounts and expiration dates.

For example:

| Coverage Amount | Policy Term |

|---|---|

| $500,000 | 10 Years |

| $300,000 | 20 Years |

| $200,000 | 30 Years |

As major financial obligations disappear, shorter policies expire naturally while longer-term protection remains in place.

This strategy can reduce costs while maintaining strong protection during your most financially vulnerable years.

Potential Downsides to Consider

While multiple policies can be beneficial, they’re not perfect.

Higher Premium Costs

More coverage usually means higher monthly premiums.

If coverage levels aren’t carefully planned, you could end up paying for insurance you don’t truly need.

More Paperwork

Managing several policies requires organization.

You’ll need to keep track of:

- Premium due dates

- Beneficiary updates

- Policy documents

- Coverage reviews

Risk of Overinsurance

Some people purchase excessive coverage simply because they qualify for it.

Money spent on unnecessary insurance might be better invested in retirement accounts, emergency funds, or other financial goals.

How Much Coverage Is Too Much?

The right amount of life insurance depends on your personal situation.

A good starting point is calculating:

- Outstanding debts

- Mortgage balance

- Children’s education costs

- Future household expenses

- Income replacement needs

- Final expenses

The goal is not to buy the maximum coverage available. The goal is to buy the amount your family would realistically need.

Frequently Asked Questions

Can I buy life insurance from multiple companies?

Yes. Many people own policies from different insurance providers.

Will beneficiaries receive money from every policy?

Generally, yes. Each valid policy can pay its death benefit separately.

Can I have both term and whole life insurance?

Absolutely. This is one of the most common life insurance strategies used today.

Is employer life insurance enough?

For many families, employer coverage alone is not sufficient because the benefit amount is often limited and tied to employment.

Do insurance companies know about my other policies?

Yes. During the application process, insurers typically ask about existing life insurance coverage.

Final Thoughts

Having multiple life insurance policies isn’t just allowed—it can be a smart financial strategy when used correctly.

Whether you’re protecting a growing family, paying off a mortgage, planning for retirement, or safeguarding a business, multiple policies can provide flexibility that a single policy may not offer.

The secret is making sure every policy serves a clear purpose. When your coverage aligns with your real financial responsibilities, multiple life insurance policies can create a powerful safety net that protects the people who matter most.

Leave a Reply