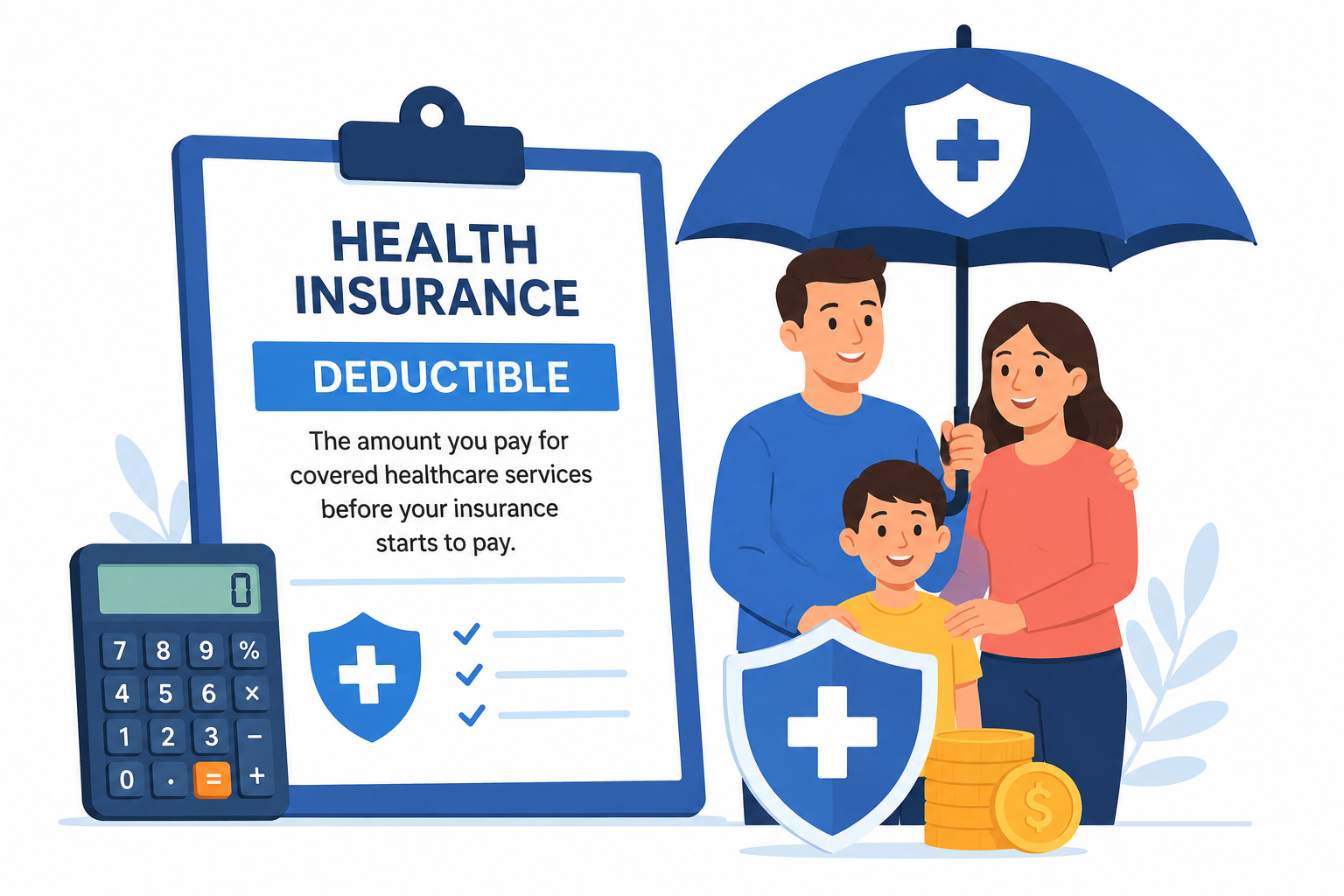

What Is a Deductible in Health Insurance?

If you’ve ever shopped for a health insurance plan, you’ve probably come across the term deductible in health insurance. While it may sound complicated, understanding your deductible is one of the most important parts of choosing the right health coverage.

Simply put, a deductible in health insurance is the amount of money you must pay out of your own pocket for covered medical services before your insurance company starts paying its share of the costs. Knowing how a deductible in health insurance works can help you estimate healthcare expenses and avoid unexpected medical bills.

Whether you’re buying insurance through your employer, the Health Insurance Marketplace, or a private insurer, understanding the role of a deductible in health insurance can help you make smarter financial decisions.

Table of Contents

- What Is a Deductible in Health Insurance?

- How Does a Deductible in Health Insurance Work?

- Example of a Health Insurance Deductible

- Types of Deductibles

- High vs. Low Deductibles

- Deductible vs. Copay

- Deductible vs. Out-of-Pocket Maximum

- How to Choose the Right Deductible

- Frequently Asked Questions

- Final Thoughts

What Is a Deductible in Health Insurance?

A deductible in health insurance is the amount you pay each year for covered healthcare services before your insurance company begins sharing the cost.

For example, if your health insurance plan has a $1,500 deductible, you’ll generally pay the first $1,500 of covered medical expenses yourself. After you meet your deductible in health insurance, your insurance company starts paying a portion of the costs according to your plan’s benefits.

The deductible resets at the beginning of each policy year for most plans.

How Does a Deductible in Health Insurance Work?

Understanding how a deductible in health insurance works is essential.

Let’s say:

- Your annual deductible is $2,000.

- You need a medical procedure costing $3,000.

In many cases:

- You pay the first $2,000.

- You’ve now met your deductible in health insurance.

- Your insurer begins paying its portion of the remaining eligible expenses.

- You may still be responsible for coinsurance or copays depending on your plan.

This is why knowing your deductible in health insurance is important when budgeting for healthcare expenses.

Example of a Health Insurance Deductible

Here’s a simple example.

Imagine you have:

- Annual deductible: $1,000

- Coinsurance: 20%

You receive medical treatment costing $5,000.

The breakdown may look like this:

- You pay the first $1,000 deductible.

- Remaining balance: $4,000.

- Insurance pays 80% of $4,000 = $3,200.

- You pay 20% of $4,000 = $800.

Total paid by you:

- Deductible: $1,000

- Coinsurance: $800

- Total: $1,800

This example shows how a deductible in health insurance affects your healthcare costs.

Types of Deductibles

Not all deductibles work the same way.

Individual Deductible

An individual deductible applies to a single covered person.

Family Deductible

A family deductible applies to everyone covered under a family health insurance plan.

Embedded Deductible

Each family member has an individual deductible within the larger family deductible.

Aggregate Deductible

The entire family deductible must be met before benefits begin for covered services.

Understanding the type of deductible in health insurance your plan uses can help avoid confusion.

High vs. Low Deductibles

When comparing plans, you’ll often see different deductible amounts.

High Deductible Health Plans

High deductible plans generally offer:

- Lower monthly premiums

- Higher out-of-pocket costs

- Eligibility for Health Savings Accounts (HSAs) in some cases

These plans may work well for healthy individuals who don’t expect frequent medical expenses.

Low Deductible Health Plans

Low deductible plans generally offer:

- Higher monthly premiums

- Lower upfront medical costs

- More predictable healthcare expenses

These plans may be beneficial for people who regularly visit doctors or take prescription medications.

Choosing the right deductible in health insurance depends on your health needs and financial situation.

Deductible vs. Copay

Many people confuse deductibles and copays.

Deductible

A deductible in health insurance is the amount you pay before insurance begins sharing costs.

Copay

A copay is a fixed amount you pay for specific services, such as:

- Doctor visits

- Specialist visits

- Prescription medications

Some preventive services may be covered before meeting your deductible.

Deductible vs. Out-of-Pocket Maximum

Another important term is the out-of-pocket maximum.

Deductible

The amount you pay before insurance starts sharing costs.

Out-of-Pocket Maximum

The maximum amount you’ll pay during a policy year for covered services.

Once you reach your out-of-pocket maximum, your insurer typically pays 100% of covered healthcare costs for the remainder of the year.

Understanding both concepts can help you evaluate the true cost of a health insurance plan.

How to Choose the Right Deductible in Health Insurance

Choosing the best deductible in health insurance depends on your circumstances.

Consider:

Your Health Status

If you rarely visit doctors, a higher deductible may save money through lower premiums.

Your Budget

Can you comfortably pay the deductible if an unexpected illness occurs?

Family Needs

Families with young children often have higher healthcare usage and may benefit from lower deductibles.

Prescription Costs

If you regularly take medications, consider plans with lower deductibles and better prescription coverage.

Emergency Savings

Having an emergency fund can make a higher deductible easier to manage.

Common Mistakes to Avoid

Many people make mistakes when evaluating a deductible in health insurance.

Common errors include:

- Choosing the lowest premium without considering the deductible.

- Ignoring out-of-pocket maximums.

- Failing to estimate annual healthcare needs.

- Confusing deductibles with copays.

- Not reviewing network restrictions.

Taking time to understand these details can save money over the long term.

Frequently Asked Questions

What is a deductible in health insurance?

A deductible in health insurance is the amount you must pay for covered healthcare services before your insurance company begins sharing costs.

Do I pay the deductible every year?

Yes. Most health insurance deductibles reset annually.

Is a higher deductible better?

A higher deductible often means lower premiums, but you’ll pay more out of pocket if you need medical care.

Do preventive services count toward the deductible?

Many health insurance plans cover preventive services before the deductible is met.

What happens after I meet my deductible?

After meeting your deductible in health insurance, your insurer typically begins paying a portion of covered medical expenses according to the plan terms.

Final Thoughts

Understanding what is a deductible in health insurance is essential for making informed healthcare decisions. Your deductible in health insurance affects both your monthly premiums and your out-of-pocket medical expenses. By comparing deductibles, premiums, and overall plan benefits, you can choose coverage that fits your healthcare needs and budget.

Before enrolling in a health insurance plan, carefully review the deductible amount and consider how it may impact your finances throughout the year.

#DeductibleInHealthInsurance #HealthCoverage #MedicalInsurance #InsuranceGuide #HealthcareCosts #InsuranceTips #PersonalFinance #HealthBenefits #HealthInsuranceExplained

Leave a Reply