📑 Table of Contents

- What Is Term Life Insurance?

- Why Term Life Insurance Is Important

- How To Buy Term Life Insurance in 7 Easy Steps

- How Much Coverage Do You Need?

- Factors That Affect Your Premium

- Common Mistakes to Avoid

- Tips to Save Money on Term Life Insurance

- Final Thoughts

- FAQ About Buying Term Life Insurance

📌 What Is Term Life Insurance?

Term life insurance is one of the simplest and most affordable forms of life insurance available today. It provides financial protection for a fixed period—commonly 10, 20, or 30 years. If the policyholder passes away during the term, the insurance company pays a predetermined amount (called the death benefit) to the beneficiaries.

Unlike permanent life insurance policies, term life insurance does not include an investment component or cash value. Its purpose is purely protection. This simplicity is exactly why it has become the most popular choice for families and individuals who want high coverage at a low cost.

For example, a young professional with a family may choose a 20-year term policy to ensure that their children’s education and household expenses are covered in case of an unexpected event.

Term life insurance is especially beneficial for:

- Parents with dependent children

- Individuals with loans or mortgages

- Breadwinners supporting their families

- Young professionals planning long-term financial security

💡 Why Term Life Insurance Is Important

Life is unpredictable, and financial planning is incomplete without life insurance. Term life insurance ensures that your loved ones are financially secure even if you are not around to support them.

Imagine a situation where your family depends on your income. Without insurance, they may struggle to manage daily expenses, pay off debts, or maintain their lifestyle. Term life insurance acts as a financial safety net.

Here are some key reasons why it is important:

Income Replacement

Your family can continue their lifestyle without financial stress.

Debt Protection

Outstanding loans like home loans, car loans, or personal loans can be paid off.

Education Funding

Your children’s education goals remain secure.

Peace of Mind

You can live stress-free knowing your family is protected.

In simple terms, term life insurance is not just a policy—it is a responsibility toward your family’s future.

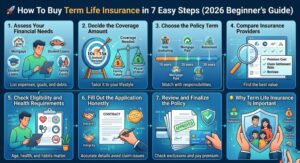

🧭 How To Buy Term Life Insurance in 7 Easy Steps

Buying term life insurance may seem complicated, but it becomes simple when broken down into clear steps.

1. Assess Your Financial Needs

The first step is understanding why you need insurance and how much protection your family requires.

Consider:

- Monthly household expenses

- Future goals (education, marriage, etc.)

- Existing savings and investments

- Outstanding debts

This step helps you calculate the financial gap your insurance needs to cover.

2. Decide the Coverage Amount

Once you understand your needs, decide how much coverage you require.

A commonly used formula is:

- 10 to 15 times your annual income

However, this is just a guideline. Your actual coverage should reflect your lifestyle, liabilities, and long-term goals.

For example, if you earn $10k annually, you may consider coverage between $10k to $30k

3. Choose the Policy Term

The policy term should align with your financial responsibilities.

Choose a term that covers:

- Your working years

- Loan repayment period

- Children’s dependency years

For most people, 20 to 30 years is an ideal term.

4. Compare Insurance Providers

Never buy a policy without comparing options. Different insurers offer different benefits and pricing.

Compare based on:

- Premium cost

- Claim settlement ratio

- Customer reviews

- Financial strength

This ensures you get the best value for your money.

5. Check Eligibility and Health Requirements

Insurance companies assess your risk before approving your policy.

Factors include:

- Age

- Health condition

- Smoking habits

- Occupation

Some policies require medical exams, while others offer no-exam options for faster approval.

6. Fill Out the Application Honestly

Always provide accurate and truthful information.

Hiding details can:

- Lead to claim rejection

- Cancel your policy

Honesty ensures your family receives the claim without complications.

7. Review and Finalize the Policy

Before purchasing, carefully review:

- Coverage amount

- Premium payment terms

- Exclusions

- Claim process

Once satisfied, complete the payment and activate your policy.

💰 How Much Coverage Do You Need?

Choosing the right coverage is one of the most important decisions when buying term life insurance.

Too little coverage may leave your family financially vulnerable, while too much coverage may increase your financial burden unnecessarily.

Here’s how to estimate your ideal coverage:

1. Calculate Annual Expenses

Multiply your yearly expenses by the number of years your family will depend on you.

2. Add Outstanding Liabilities

Include loans, credit cards, and other debts.

3. Include Future Goals

Consider children’s education, marriage, and other long-term plans.

4. Subtract Existing Assets

Deduct savings, investments, and existing insurance.

This calculation gives you a realistic coverage amount tailored to your needs.

💸 Factors That Affect Your Premium

Your premium is influenced by several factors. Understanding these can help you reduce your costs.

Age

Younger applicants pay lower premiums.

Health Condition

Healthy individuals get better rates.

Lifestyle Habits

Smoking and alcohol consumption increase premiums.

Occupation

High-risk jobs may lead to higher costs.

Coverage Amount

Higher coverage means higher premium.

Policy Term

Longer terms usually cost more but offer extended protection.

Maintaining a healthy lifestyle and buying early can significantly lower your premium.

⚠️ Common Mistakes to Avoid

Many people make mistakes while buying life insurance, which can lead to financial loss.

Not Comparing Policies

Always explore multiple options before deciding.

Choosing Cheapest Plan Only

Low cost may mean limited benefits.

Ignoring Policy Terms

Understand exclusions and conditions clearly.

Delaying Purchase

Premiums increase with age.

Providing Incorrect Information

This can result in claim rejection.

Avoiding these mistakes ensures you make a smart and secure decision.

💡 Tips to Save Money on Term Life Insurance

If you want to reduce your premium without compromising coverage, follow these tips:

- Buy at a younger age

- Maintain a healthy lifestyle

- Avoid smoking

- Compare multiple insurers

- Choose only the required coverage

- Opt for longer-term policies

These simple strategies can save you a significant amount over the life of your policy.

🔥 Final Thoughts

Buying term life insurance is not just a financial decision—it is a responsibility toward your loved ones. It ensures that your family remains financially stable even in your absence.

By following these 7 easy steps, you can simplify the process and make an informed decision. The key is to start early, choose wisely, and stay consistent.

Remember, the best time to buy life insurance is today. Waiting only increases costs and risks.

Take action now and secure your family’s future with confidence.

❓ FAQ About Buying Term Life Insurance

Q1. What is the best age to buy term life insurance?

The earlier you buy, the lower your premium will be.

Q2. Can I buy term life insurance online?

Yes, most insurers offer a fully digital process.

Q3. Do I need a medical exam?

Not always. Many insurers provide no-exam policies.

Q4. What happens if I outlive my policy?

The policy expires, and no payout is made.

Q5. Can I cancel my policy anytime?

Yes, but terms vary by insurer.

Q6. How long does approval take?

It can be instant or take a few days.

Q7. Is term life insurance enough?

For most people, yes—it provides essential financial protection at an affordable cost.