Colorado Insurance Rates Are Exploding—Here’s Why

Table of Contents

- The Reality: Why Everyone Is Talking About Colorado Insurance

- What’s Driving the Sudden Price Surge

- Wildfires: The Biggest Cost Factor

- Hailstorms and Severe Weather Damage

- Rising Rebuilding Costs and Inflation

- Why Insurance Companies Are Tightening Rules

- Hidden Policy Changes Most Homeowners Miss

- How Much Rates Have Increased (Real Trends)

- Who Is Being Hit the Hardest

- Are Homes Becoming Uninsurable?

- How to Protect Yourself from Rising Costs

- Smart Ways to Lower Your Premium

- Mistakes That Make Insurance Even More Expensive

- What the Future Looks Like in Colorado

- FAQs

- Conclusion

The Reality: Why Everyone Is Talking About Colorado Insurance

Homeowners across Colorado are facing a harsh new reality—insurance is no longer predictable or affordable.

Premiums are rising faster than most people expected, and in some cases, homeowners are seeing double-digit increases year after year. What used to be a routine expense is now becoming a major financial burden.

The shocking part? This trend is not temporary—it’s part of a larger shift in how insurance works in high-risk states.

What’s Driving the Sudden Price Surge

Insurance rates don’t increase randomly. They rise when risk increases—and Colorado’s risk profile has changed dramatically.

Several key factors are pushing prices higher at the same time:

- More frequent natural disasters

- Higher claim payouts

- Rising construction and repair costs

- Increasing reinsurance expenses

When insurers face higher costs, they pass those costs on to homeowners.

Wildfires: The Biggest Cost Factor

Wildfires are one of the main reasons insurance rates are skyrocketing in Colorado.

Over the past few years, fires have become more intense, more destructive, and less predictable. Areas that were once considered safe are now being reclassified as high-risk zones.

For insurance companies, this means massive potential losses. For homeowners, it means higher premiums—or difficulty getting coverage at all.

Hailstorms and Severe Weather Damage

Colorado is one of the most hail-prone states in the USA.

Hailstorms cause billions of dollars in damage each year, especially to roofs, vehicles, and property exteriors. Even small storms can result in widespread claims.

Because hail damage is so frequent and costly, insurers are adjusting their policies—often by increasing deductibles or limiting coverage.

Rising Rebuilding Costs and Inflation

Even without disasters, insurance costs would still be rising due to inflation.

Construction materials, labor, and supply chain disruptions have significantly increased rebuilding costs. If your home is damaged, it now costs much more to repair or rebuild it than it did just a few years ago.

Insurance premiums must reflect these higher costs.

Why Insurance Companies Are Tightening Rules

To manage risk, insurance companies are becoming more selective.

They are tightening underwriting standards, increasing deductibles, and in some cases, refusing to insure certain properties altogether.

Homes in wildfire-prone areas or with older roofs may face higher premiums or limited coverage options.

Hidden Policy Changes Most Homeowners Miss

One of the biggest problems is not just rising prices—it’s changing coverage.

Many policies now include:

- Higher deductibles for wind and hail damage

- Roof depreciation clauses

- Stricter claim conditions

These changes are often buried in policy details, meaning homeowners don’t notice them until they file a claim.

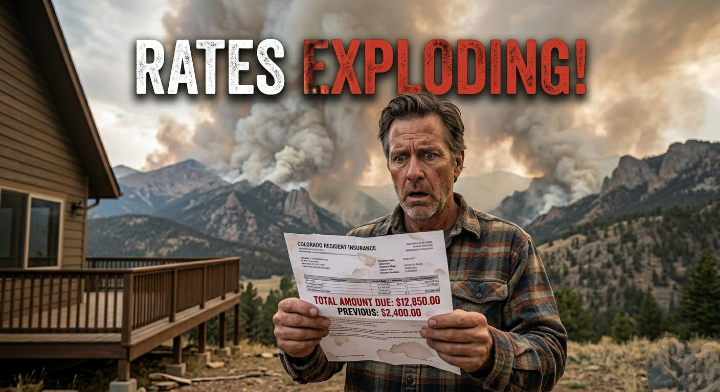

How Much Rates Have Increased (Real Trends)

While exact increases vary, many Colorado homeowners are seeing premiums rise by 20% to 50% or more.

In high-risk areas, the increase can be even higher. Some homeowners are also experiencing policy non-renewals, forcing them to find more expensive alternatives.

Who Is Being Hit the Hardest

Not all homeowners are affected equally.

Those living in wildfire-prone zones, areas with frequent hailstorms, or homes with older construction are facing the biggest increases.

New homeowners are also struggling, as higher insurance costs add to already expensive housing prices.

Are Homes Becoming Uninsurable?

In some cases, yes.

Certain properties are now considered too risky for private insurers. This is especially true in areas with repeated wildfire damage or extreme weather exposure.

When this happens, homeowners may have limited options and higher costs.

How to Protect Yourself from Rising Costs

You can’t control the market, but you can control how prepared you are.

Start by reviewing your policy carefully. Understand your coverage limits, deductibles, and exclusions.

Improving your home’s resilience—such as upgrading your roof or creating defensible space—can reduce risk and make your property more attractive to insurers.

Smart Ways to Lower Your Premium

There are practical ways to reduce your insurance costs:

- Bundle policies (home + auto)

- Increase your deductible (if financially manageable)

- Install safety and security features

- Shop around and compare providers

Small changes can make a significant difference over time.

Mistakes That Make Insurance Even More Expensive

One common mistake is ignoring policy updates. Insurance terms change, and failing to review them can lead to unexpected costs.

Another mistake is choosing the cheapest policy without understanding coverage. Lower premiums often mean higher risk.

Delaying home maintenance can also increase your premium or lead to claim denials.

What the Future Looks Like in Colorado

Insurance in Colorado is entering a new phase.

We can expect continued rate increases, stricter policies, and more advanced risk assessments. Climate trends and economic factors will continue to shape the market.

Homeowners who stay informed and proactive will be in the best position to adapt.

FAQs

Why are insurance rates rising in Colorado?

Due to wildfires, hailstorms, and higher repair costs.

Can I still find affordable insurance?

Yes, but it requires comparison and risk management.

What increases my premium the most?

Location, home condition, and claim history.

Are policies becoming stricter?

Yes, insurers are tightening coverage to manage risk.

How can I reduce my costs?

Improve home safety and review your policy regularly.

Conclusion

Colorado’s insurance market is changing fast—and not in favor of homeowners.

Rising risks, higher costs, and stricter policies are creating a challenging environment. The days of cheap, predictable insurance are fading.

But this doesn’t mean you’re powerless.

By understanding why rates are increasing and taking proactive steps, you can protect both your home and your finances.

Because in today’s market, the smartest homeowners aren’t just insured—they’re informed.