I Thought I Was Covered… Then a $120,000 Bill Arrived: The Truth About US Health Insurance

Table of Contents

- A Real Scenario: How One Bill Changes Everything

- Why “Covered” Doesn’t Mean What You Think

- Understanding the Basics (Deductibles, Copays, Coinsurance)

- The Hidden Gaps That Create Massive Bills

- Out-of-Network Charges: The Silent Budget Killer

- Emergency Care Doesn’t Always Mean Full Coverage

- The Fine Print Most People Never Read

- Balance Billing: The $120,000 Shock Explained

- How Claims Get Reduced or Denied

- Real Financial Impact on Families

- How to Protect Yourself Before a Medical Crisis

- What to Do If You Receive a Huge Medical Bill

- Common Mistakes That Lead to Financial Disaster

- Future of Health Insurance in the USA

- FAQs

- Conclusion

A Real Scenario: How One Bill Changes Everything

Imagine this.

You have health insurance. You pay your monthly premium. You believe you’re protected. Then one day, an emergency happens—a surgery, an accident, or a sudden illness.

Weeks later, a bill arrives: $120,000.

Your first reaction? “This must be a mistake. I’m insured.”

But it’s not always a mistake. This situation is more common than most Americans realize.

Why “Covered” Doesn’t Mean What You Think

Health insurance doesn’t mean everything is fully paid.

It means your costs are shared with the insurance company—under specific rules. These rules include deductibles, network restrictions, coverage limits, and exclusions.

If you don’t understand these rules, you could face massive unexpected costs.

Understanding the Basics (Deductibles, Copays, Coinsurance)

To understand why bills get so high, you need to know how cost-sharing works.

A deductible is what you pay before insurance starts covering expenses.

Copays are fixed amounts you pay for services, like doctor visits.

Coinsurance is the percentage of costs you share after meeting your deductible.

Even with insurance, these costs can add up quickly—especially during major medical events.

The Hidden Gaps That Create Massive Bills

Most policies include gaps that are not obvious at first glance.

Some treatments may not be fully covered. Certain procedures may require pre-approval. There may be limits on how much the insurer will pay for specific services.

These gaps are often buried in policy documents, which many people never read in detail.

Out-of-Network Charges: The Silent Budget Killer

One of the biggest reasons for massive medical bills is out-of-network care.

If you receive treatment from a provider outside your insurance network, your insurer may cover only a small portion—or nothing at all.

This can happen even in hospitals that are considered “in-network” if certain doctors or specialists are not.

Emergency Care Doesn’t Always Mean Full Coverage

Many people assume emergencies are fully covered.

While insurance often covers emergency services, it doesn’t guarantee full payment. Follow-up care, specialist treatment, or extended hospital stays may fall outside coverage limits or networks.

This is where costs can spiral quickly.

The Fine Print Most People Never Read

Insurance policies are detailed legal documents.

They include exclusions, limitations, and conditions that affect how claims are processed. These details are rarely emphasized but can have a huge financial impact.

Ignoring the fine print is one of the most common—and costly—mistakes.

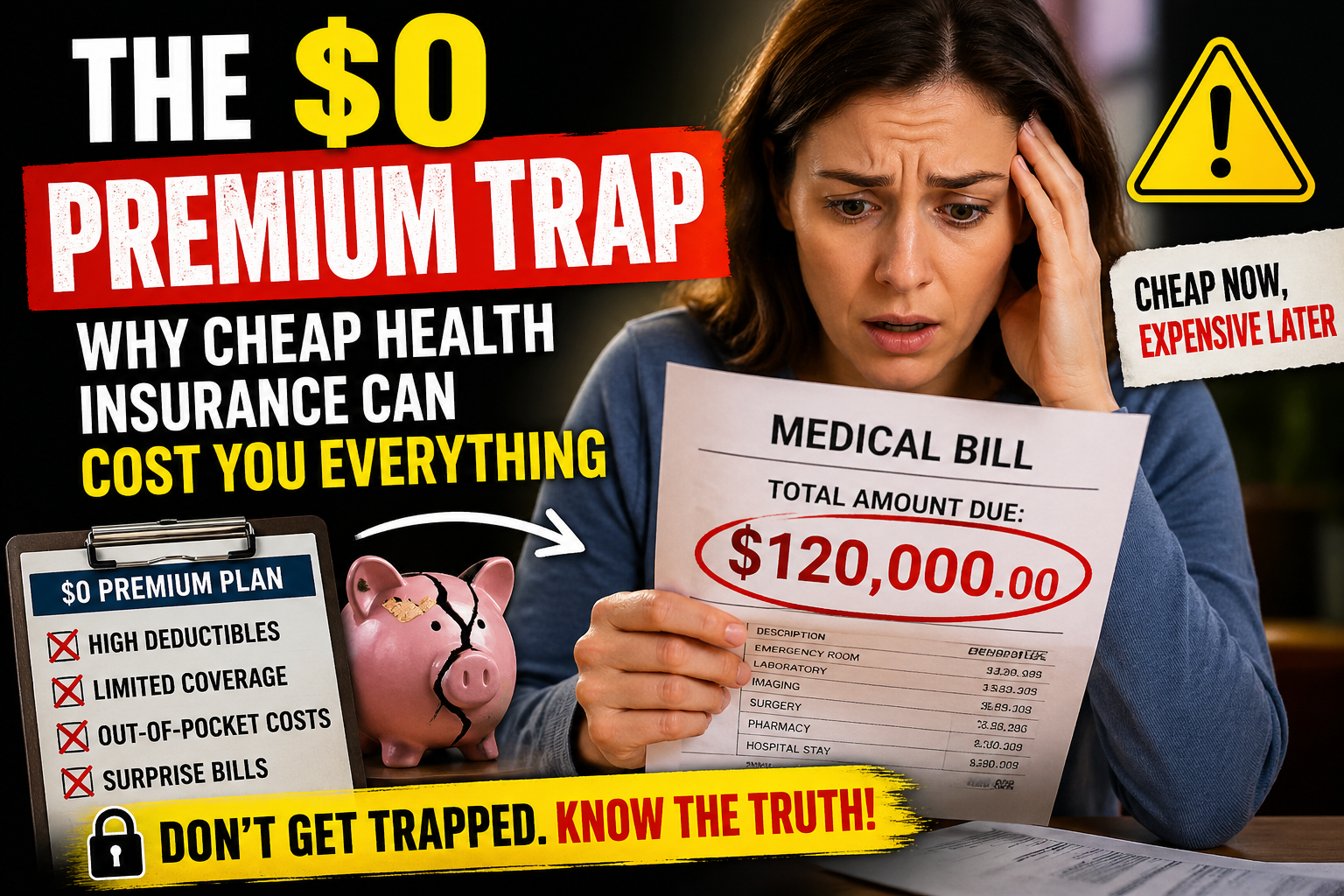

Balance Billing: The $120,000 Shock Explained

Balance billing occurs when a healthcare provider charges you the difference between what your insurance pays and the total cost of care.

For example, if a provider charges $150,000 and your insurer pays $30,000, you could be billed for the remaining $120,000.

This is one of the main reasons patients receive unexpectedly large bills.

How Claims Get Reduced or Denied

Not all claims are paid in full. Some are reduced or denied entirely.

Common reasons include:

- Services not covered by the policy

- Lack of pre-authorization

- Out-of-network providers

- Documentation issues

Even partial denials can lead to significant out-of-pocket costs.

Real Financial Impact on Families

Medical debt is one of the leading causes of financial stress in the United States.

Unexpected bills can drain savings, increase debt, and create long-term financial challenges.

For many families, a single medical event can change their financial future.

How to Protect Yourself Before a Medical Crisis

Preparation is your best defense.

Understand your policy in detail—especially your network, deductibles, and coverage limits.

Whenever possible, confirm that providers are in-network before receiving care.

Keep records of all medical visits, approvals, and communications with your insurer.

What to Do If You Receive a Huge Medical Bill

If you receive a large bill, don’t panic—but don’t ignore it either.

Review the bill carefully for errors. Request an itemized statement and compare it with your insurance explanation of benefits.

You can also contact your insurer to clarify charges and appeal decisions if necessary.

In some cases, negotiating with providers or setting up payment plans can reduce the financial burden.

Common Mistakes That Lead to Financial Disaster

One major mistake is assuming all providers at a hospital are in-network.

Another is not understanding your deductible and out-of-pocket maximum.

Ignoring insurance communications or failing to follow required procedures can also lead to denied claims.

Future of Health Insurance in the USA

The health insurance system is evolving, but challenges remain.

Efforts to increase transparency and reduce unexpected billing are ongoing, but gaps still exist.

Patients will need to stay informed and proactive to avoid financial surprises.

FAQs

Why did I get a huge bill even with insurance?

Due to out-of-network care, coverage limits, or cost-sharing.

What is balance billing?

Charging the patient the difference between provider cost and insurer payment.

Can I dispute a medical bill?

Yes, you can request corrections or appeal decisions.

How can I avoid large bills?

Understand your policy and stay within your network.

Is emergency care fully covered?

Not always—follow-up costs may not be fully covered.

Conclusion

The biggest myth about health insurance is that it guarantees full protection.

In reality, it’s a complex system with rules, limits, and gaps that can lead to massive unexpected costs.

A $120,000 bill isn’t just a shocking number—it’s a wake-up call.

Understanding your insurance is not optional—it’s essential.

Because when it comes to healthcare, what you don’t know can cost you the most.