Most homeowners think their insurance price depends mainly on the size of their house.

But in reality, your ZIP code can change your premium by thousands of dollars every year.

Two homes with similar value can have completely different insurance costs simply because they are located in different areas. One neighborhood may have low storm risk and fewer claims, while another ZIP code just a few miles away could face hurricanes, wildfires, theft, or expensive rebuilding costs.

That’s why insurance companies pay extremely close attention to location.

In 2026, homeowners across America are seeing insurance prices rise sharply in certain ZIP codes while other areas continue to stay surprisingly affordable.

This guide compares average home insurance costs by ZIP code across the United States and explains why some locations pay far more than others.

Jump To

- Why ZIP Codes Affect Home Insurance Prices

- How Insurance Companies Calculate Risk

- Average Home Insurance Costs by ZIP Code

- The Cheapest ZIP Codes for Home Insurance

- The Most Expensive Areas for Coverage

- Why Neighboring ZIP Codes Can Have Different Rates

- How Weather Disasters Affect Insurance Costs

- Ways Homeowners Are Lowering Their Premiums

- What Most Homeowners Forget to Check

- Final Thoughts

- FAQs

Why ZIP Codes Affect Home Insurance Prices

Insurance companies look at much more than your home itself.

Your location tells insurers how risky your property may be.

Factors Insurance Companies Study

Your ZIP code may affect:

- Storm and hurricane exposure

- Wildfire risk

- Flood probability

- Crime rates

- Local rebuilding costs

- Fire department access

- Past insurance claims in the area

Even neighboring ZIP codes can have very different insurance prices because risk levels change quickly from one area to another.

How Insurance Companies Calculate Risk

Insurance pricing is based on probability.

The higher the chance of future claims, the higher the premium usually becomes.

Why Some Areas Pay More

Homes in regions exposed to:

- Hurricanes

- Tornadoes

- Severe hail

- Flooding

- Wildfires

often see much higher insurance costs than homes in lower-risk locations.

For example, coastal states and disaster-prone areas frequently pay far above the national average.

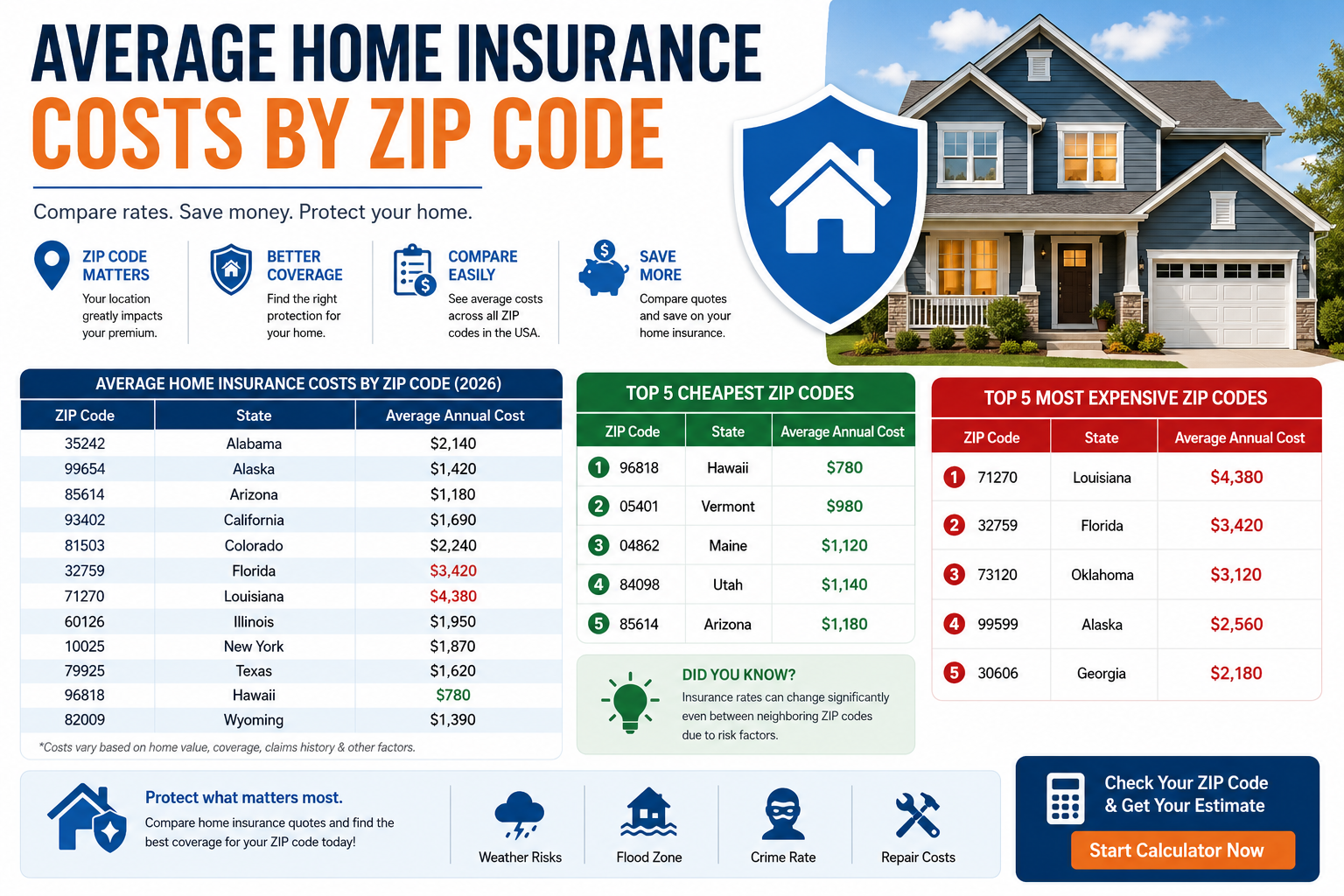

Average Home Insurance Costs by ZIP Code

Below are estimated average annual home insurance costs for selected ZIP codes across different states in the United States.

| ZIP Code | State | Estimated Average Annual Cost |

|---|---|---|

| 35242 | Alabama | $2,140 |

| 99654 | Alaska | $1,420 |

| 85614 | Arizona | $1,180 |

| 72745 | Arkansas | $2,010 |

| 93402 | California | $1,690 |

| 81503 | Colorado | $2,240 |

| 06790 | Connecticut | $1,560 |

| 19808 | Delaware | $1,340 |

| 20011 | District of Columbia | $1,510 |

| 32759 | Florida | $3,420 |

| 30606 | Georgia | $2,180 |

| 96818 | Hawaii | $780 |

| 60126 | Illinois | $1,950 |

| 46528 | Indiana | $1,720 |

| 52253 | Iowa | $1,860 |

| 66030 | Kansas | $2,480 |

| 41075 | Kentucky | $2,020 |

| 71270 | Louisiana | $4,380 |

| 04862 | Maine | $1,120 |

| 20895 | Maryland | $1,640 |

| 01267 | Massachusetts | $1,430 |

| 48109 | Michigan | $1,980 |

| 55901 | Minnesota | $2,120 |

| 39305 | Mississippi | $2,960 |

| 63141 | Missouri | $2,130 |

| 59715 | Montana | $1,470 |

| 68114 | Nebraska | $2,040 |

| 89511 | Nevada | $1,290 |

| 03062 | New Hampshire | $1,090 |

| 07030 | New Jersey | $1,920 |

| 87111 | New Mexico | $1,540 |

| 10025 | New York | $1,870 |

| 27514 | North Carolina | $2,060 |

| 58104 | North Dakota | $1,730 |

| 44113 | Ohio | $1,690 |

| 73120 | Oklahoma | $3,120 |

| 97229 | Oregon | $1,280 |

| 19087 | Pennsylvania | $1,760 |

| 02906 | Rhode Island | $1,590 |

| 29205 | South Carolina | $2,420 |

| 57108 | South Dakota | $1,880 |

| 37205 | Tennessee | $2,240 |

| 79925 | Texas | $1,620 |

| 84098 | Utah | $1,140 |

| 05401 | Vermont | $980 |

| 22030 | Virginia | $1,520 |

| 98052 | Washington | $1,340 |

| 53217 | Wisconsin | $1,480 |

| 82009 | Wyoming | $1,390 |

The Cheapest ZIP Codes for Home Insurance

Some ZIP codes consistently stay below the national average.

Why Certain Areas Pay Less

Lower premiums are often found in places with:

- Low disaster risk

- Fewer insurance claims

- Mild weather patterns

- Lower rebuilding costs

- Strong local fire protection

Areas in Hawaii, Vermont, Utah, and parts of New Hampshire often see lower-than-average premiums compared to coastal hurricane states.

The Most Expensive Areas for Coverage

Some homeowners now pay several thousand dollars yearly just for insurance.

States With Higher Costs

Areas commonly facing higher premiums include:

- Florida

- Louisiana

- Oklahoma

- Coastal Texas

- Hurricane-prone Gulf Coast regions

Frequent storms and expensive claims continue pushing premiums upward in these areas.

Why Neighboring ZIP Codes Can Have Different Rates

Many homeowners are shocked when nearby neighborhoods pay completely different insurance prices.

Why Small Distance Changes Matter

Insurance companies analyze:

- Local crime statistics

- Fire station distance

- Flood maps

- Claim history

- Property values

A home located closer to wildfire zones or flood-prone areas may pay dramatically more even within the same city.

How Weather Disasters Affect Insurance Costs

Extreme weather has become one of the biggest reasons premiums continue rising nationwide.

Weather Events Increasing Costs

Major disasters affecting rates include:

- Hurricanes

- Tornadoes

- Hailstorms

- Flooding

- Wildfires

- Winter freezes

As insurance payouts increase, companies often raise premiums across affected regions.

Ways Homeowners Are Lowering Their Premiums

Many homeowners are actively searching for ways to reduce rising insurance costs.

Common Money-Saving Strategies

Homeowners often save by:

- Bundling home and auto insurance

- Installing security systems

- Raising deductibles carefully

- Improving roofs and wiring

- Comparing quotes yearly

- Avoiding small unnecessary claims

Even small discounts can reduce yearly costs significantly.

What Most Homeowners Forget to Check

Price matters, but coverage matters even more.

Common Coverage Mistakes

Some homeowners forget to review:

- Flood exclusions

- Replacement cost limits

- Deductible structures

- Jewelry coverage limits

- Roof damage clauses

- Water backup protection

Many only notice coverage gaps after major damage happens.

Final Thoughts

Your ZIP code may influence your home insurance premium more than almost any other factor.

That’s why homeowners living only a few miles apart can end up paying completely different prices for similar homes.

As weather risks, rebuilding costs, and claim expenses continue rising across the United States, location-based pricing is becoming even more important in 2026.

The smartest homeowners are not only comparing prices — they are also comparing coverage quality, disaster protection, and policy details carefully before choosing insurance.

Because when severe damage happens, the cheapest policy is not always the best one.

FAQs

Why does ZIP code affect home insurance rates?

Insurance companies use ZIP codes to estimate local risk levels including storms, crime, fires, and past claims.

Which states have the highest home insurance costs?

Florida, Louisiana, Oklahoma, and some Gulf Coast regions often have the highest premiums.

Can two nearby homes have different insurance prices?

Yes. Flood zones, crime rates, and property risks can vary significantly even between nearby ZIP codes.

Is home insurance getting more expensive in 2026?

In many parts of the U.S., yes. Weather disasters and rebuilding costs continue pushing premiums higher.

How can homeowners lower insurance costs?

Bundling policies, improving home safety, comparing quotes, and choosing higher deductibles carefully may help reduce premiums.

Leave a Reply