Electric bikes and scooters are everywhere in New York now.

From busy Manhattan streets to quiet Brooklyn neighborhoods, thousands of commuters are replacing cars and subways with faster, cheaper electric rides. E-bikes and electric scooters save fuel, avoid traffic, and make city travel far more convenient.

But one unexpected accident can create a financial disaster many riders never see coming.

A pedestrian injury, damaged vehicle, or stolen e-bike could suddenly leave someone paying thousands out of pocket. And that raises one important question many New Yorkers are asking in 2026:

Do you actually need separate insurance for an e-bike or electric scooter in New York?

The answer is more complicated than most riders think.

Some e-bikes may already have limited coverage under existing insurance policies. Certain electric scooters may not. And many riders only discover the gaps after an accident happens.

This guide explains New York’s current rules, hidden insurance risks, and what riders should know before assuming they are fully protected.

Jump To

- Are E-Bikes and Electric Scooters Legal in New York?

- Do You Legally Need Insurance in New York?

- What Standard Insurance Policies Usually Cover

- The Biggest Insurance Gaps Most Riders Ignore

- When Separate E-Bike Insurance Makes Sense

- Electric Scooter Insurance Risks

- How Much E-Bike Insurance Costs in New York

- What Riders Should Look for in Coverage

- Common Mistakes New York Riders Make

- Final Thoughts

- FAQs

Are E-Bikes and Electric Scooters Legal in New York?

New York officially legalized certain e-bikes and electric scooters in recent years, which dramatically increased their popularity across the state.

Today many delivery workers, students, and commuters rely on electric transportation daily.

Types of E-Bikes Allowed in New York

New York generally recognizes multiple classes of e-bikes including:

- Class 1 e-bikes with pedal assist

- Class 2 e-bikes with throttle assistance

- Faster Class 3 commuter-style e-bikes

However speed limits and local restrictions may vary depending on the city or road type.

Why Legal Status Matters for Insurance

Insurance companies often treat electric bikes differently depending on their speed, motor power, and classification.

A low-speed pedal-assist bike may receive limited coverage under existing homeowners or renters insurance. A faster high-powered e-bike may not.

That difference becomes extremely important after accidents or theft claims.

Do You Legally Need Insurance in New York?

Many New Yorkers assume e-bikes work like motorcycles when it comes to insurance requirements.

In most cases that is not true.

Current New York Requirements

Most standard e-bikes and electric scooters currently do not require:

- Vehicle registration

- License plates

- Mandatory liability insurance

That makes them easier and cheaper to own compared to cars or motorcycles.

Why “Not Required” Does Not Mean “Protected”

Even though separate insurance may not be legally required, riders can still face major financial liability after accidents.

If an e-bike rider injures someone or damages property, the rider may still be personally responsible for medical bills, legal costs, or repairs.

That is where insurance becomes important.

What Standard Insurance Policies Usually Cover

Some riders already have limited protection through existing policies without realizing it.

But coverage gaps are extremely common.

Homeowners and Renters Insurance

Certain homeowners or renters insurance policies may help cover:

- E-bike theft

- Fire damage

- Limited personal property losses

However many insurers exclude high-powered electric bikes entirely.

Some policies also refuse claims if the e-bike exceeds specific speed or wattage limits.

Auto Insurance Usually Does Not Apply

Most standard car insurance policies do not automatically cover e-bikes or electric scooters.

Many riders incorrectly assume their auto liability policy extends protection automatically.

Often it does not.

The Biggest Insurance Gaps Most Riders Ignore

The biggest financial danger is liability coverage.

Accident Liability Risks

Imagine a rider accidentally hits:

- A pedestrian crossing the street

- A parked luxury vehicle

- Another cyclist

- A delivery worker

- Public property

Without liability protection the rider could face lawsuits or expensive settlements personally.

Theft Is Also a Growing Problem

E-bike theft has become increasingly common across New York City.

High-end electric bikes can cost several thousand dollars, making them attractive targets for thieves.

Many riders only discover insurance exclusions after the bike disappears.

When Separate E-Bike Insurance Makes Sense

Separate e-bike insurance becomes more valuable as the bike itself becomes more expensive or heavily used.

Riders Who May Need Extra Coverage

Separate policies may make sense for:

- Daily commuters

- Delivery drivers

- Owners of expensive e-bikes

- Riders traveling long distances

- Riders storing bikes outdoors frequently

Specialized e-bike insurance may include liability, theft, crash damage, roadside assistance, and medical payments.

Why Delivery Riders Face Higher Risk

Commercial use often changes insurance rules completely.

Some personal insurance policies may deny claims if the e-bike was being used for deliveries or business purposes during the accident.

That loophole surprises many gig workers.

Electric Scooter Insurance Risks

Electric scooters create similar insurance questions but often involve even more uncertainty.

Why Scooters Can Be Complicated

Scooter classifications vary widely depending on:

- Maximum speed

- Motor size

- Local regulations

- Road usage

Some insurers treat faster scooters more like mopeds than bicycles.

Shared Scooter Services vs Personal Ownership

Rental scooter companies may provide limited liability coverage while the ride is active.

But personal scooters may require entirely different protection depending on the insurer.

Coverage differences can become confusing quickly.

How Much E-Bike Insurance Costs in New York

The good news is that separate e-bike insurance is usually far cheaper than car insurance.

Factors That Affect Cost

Insurance pricing often depends on:

- Bike value

- Rider location

- Theft risk

- Coverage limits

- Riding frequency

- Commercial usage

Higher-end bikes in dense urban areas like New York City may cost more to insure because theft rates are higher.

Why Some Riders Skip Coverage

Many riders avoid insurance to save money upfront.

But replacing a stolen $4,000 e-bike or paying injury claims after an accident could cost far more later.

What Riders Should Look for in Coverage

Not all e-bike policies provide the same protection.

Important Coverage Features

Riders should compare policies carefully for:

- Theft protection

- Liability coverage

- Crash damage coverage

- Medical payments

- Roadside assistance

- Worldwide or travel coverage

Understanding exclusions is just as important as understanding benefits.

Why Reading the Fine Print Matters

Some policies exclude:

- Commercial delivery use

- Racing activities

- Unlocked bikes

- High-speed modifications

These exclusions can completely change whether a claim gets approved.

Common Mistakes New York Riders Make

Many riders unknowingly expose themselves to major financial risk.

Common Insurance Mistakes

Frequent mistakes include:

- Assuming renters insurance covers everything

- Never checking liability protection

- Ignoring theft exclusions

- Using personal coverage for delivery work

- Failing to document bike ownership

- Forgetting to record serial numbers

Small oversights can create expensive consequences after accidents or theft.

Final Thoughts

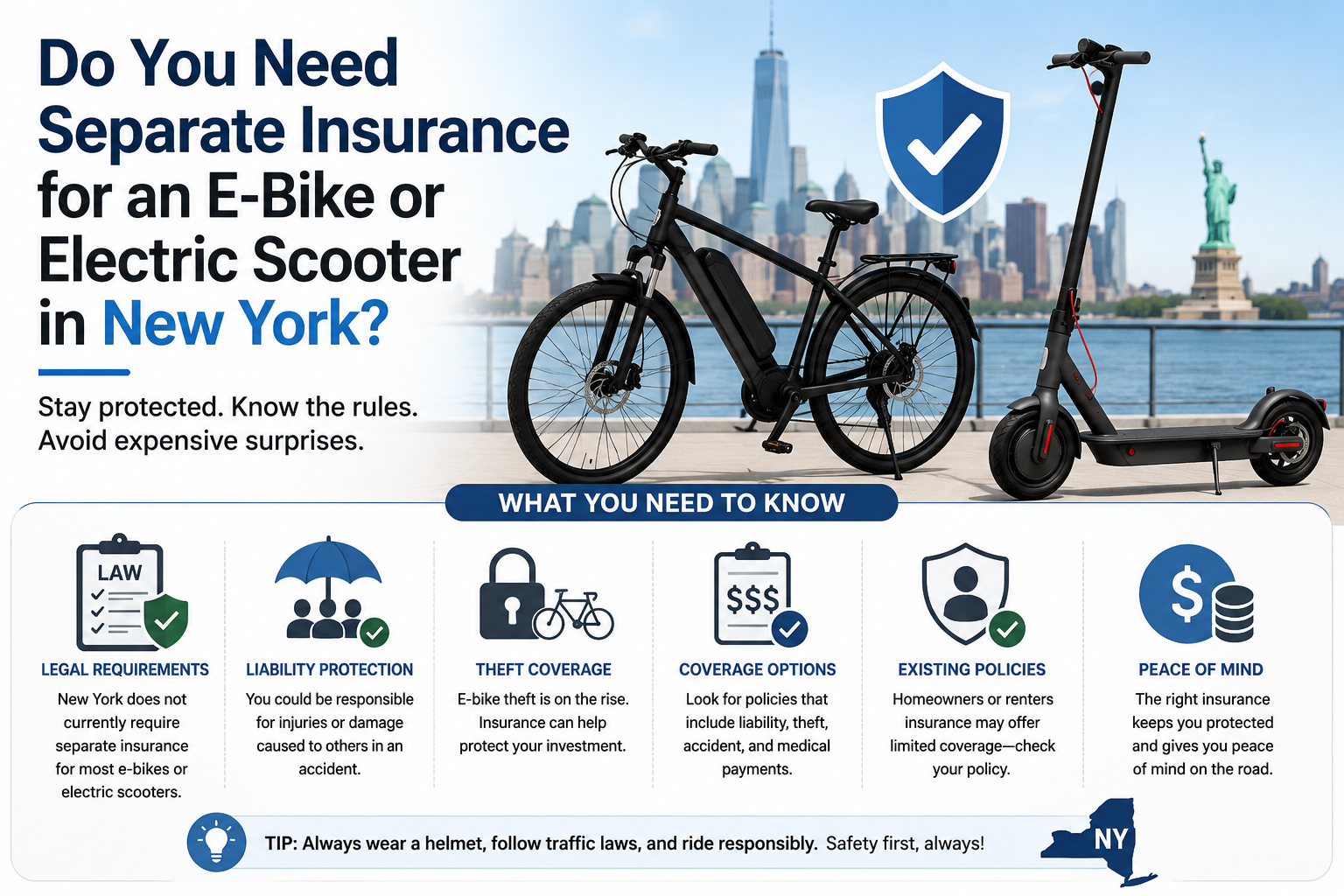

New York does not currently require separate insurance for most e-bikes and electric scooters.

But that does not mean riders are automatically protected financially.

As e-bikes become faster, more expensive, and more common across New York streets, insurance gaps are becoming increasingly important. One serious accident or theft could easily cost more than the bike itself.

For many riders, separate e-bike insurance is less about legal requirements and more about protecting themselves from financial surprises they never expected.

Understanding coverage before an accident happens can make a massive difference later.

FAQs

Is e-bike insurance mandatory in New York?

Most standard e-bikes currently do not legally require separate insurance in New York.

Does renters insurance cover stolen e-bikes?

Sometimes, but coverage limits and exclusions vary significantly between insurers.

Are electric scooters insured under car insurance?

Usually not. Most auto insurance policies do not automatically cover personal electric scooters.

Do delivery riders need separate insurance?

Often yes. Commercial delivery use may be excluded from personal policies.

Is e-bike insurance expensive?

Usually it costs much less than car insurance, though pricing depends on the bike value and coverage type.

Leave a Reply