If you’ve opened your homeowners insurance renewal notice this year and wondered, “Why did my premium go up again?”, you’re not alone. Across the United States, millions of homeowners are seeing higher insurance bills in 2026—even if they’ve never filed a claim. It’s frustrating to pay more for the same coverage, especially when nothing about your home has changed. But the reality is that homeowners insurance premiums are influenced by far more than your personal claims history.

Insurance companies calculate premiums based on overall risk. That means rising construction costs, severe weather, inflation, labor shortages, and increasing claim payouts all affect what homeowners pay. Understanding why homeowners insurance rates keep rising in 2026 can help you make smarter decisions about your policy and identify ways to reduce your costs without sacrificing valuable coverage.

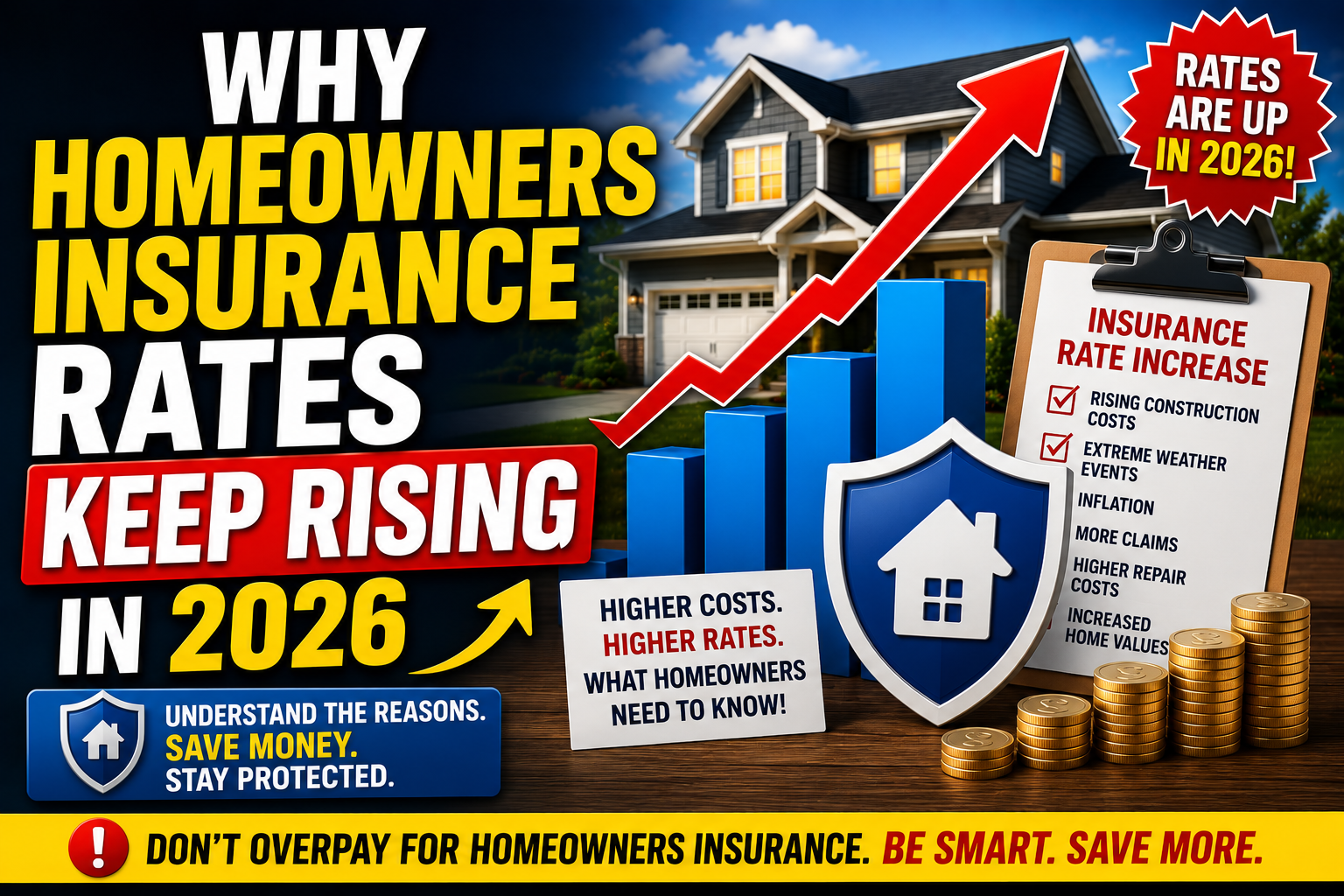

One of the biggest reasons homeowners insurance rates continue to increase is the rising cost of rebuilding homes. Construction materials such as lumber, concrete, roofing shingles, insulation, windows, and electrical supplies remain expensive compared to previous years. At the same time, skilled labor costs have increased as contractors charge more for repairs and rebuilding projects. Because homeowners insurance is designed to cover the cost of rebuilding your home after a covered loss, insurers must adjust coverage limits and premiums to reflect these higher expenses.

Another major factor is the growing number of extreme weather events across the country. Hurricanes, tornadoes, hailstorms, wildfires, severe thunderstorms, flooding, and winter storms have become more frequent and more costly. Even if your own home has never been damaged, insurance companies spread the financial risk across all policyholders. As catastrophic claims increase nationwide, premiums often rise for everyone.

Inflation also plays a significant role. Nearly every part of repairing or replacing a home costs more in 2026 than it did just a few years ago. Building materials, transportation, equipment, temporary housing, and repair services have all become more expensive. Since insurance companies must pay these higher costs when settling claims, premiums naturally increase to keep pace.

Many homeowners are surprised to learn that their neighbors’ claims can affect their own insurance rates. Insurance companies evaluate claim activity across neighborhoods, ZIP codes, and entire states. If an area experiences frequent storm damage, theft, vandalism, or water damage claims, insurers may view that location as higher risk, leading to increased homeowners insurance premiums for everyone nearby.

Another reason for rising rates is the increasing number of expensive water damage claims. Burst pipes, leaking appliances, sewer backups, and hidden plumbing failures can cause thousands of dollars in repairs. Water damage has become one of the most common homeowners insurance claims, prompting insurers to raise premiums and encourage homeowners to install smart leak detection systems and automatic shut-off devices.

Home values have also increased in many parts of the United States. While a higher home value may be good news for homeowners, it often means higher replacement costs. Larger homes, upgraded kitchens, luxury flooring, custom cabinetry, and premium finishes require more expensive repairs after a covered loss, increasing the amount insurers may have to pay.

Insurance companies themselves are facing higher operating costs. Claim processing, customer service, technology investments, fraud prevention, and regulatory compliance all require significant resources. These business expenses can contribute to higher premiums over time.

In some states, legal costs and insurance fraud have become growing concerns. Fraudulent claims, inflated repair estimates, and lengthy legal disputes increase the overall cost of doing business for insurers. Those additional expenses are often reflected in higher homeowners insurance premiums for policyholders.

Although homeowners cannot control inflation or severe weather, there are several practical ways to reduce insurance costs. Comparing homeowners insurance quotes from multiple companies before each renewal is one of the most effective strategies. Insurance companies evaluate risk differently, meaning similar coverage may cost significantly less with another insurer.

Bundling homeowners insurance with auto insurance is another popular way to save money. Many insurers offer multi-policy discounts that can substantially reduce annual premiums. Installing monitored security systems, smoke detectors, impact-resistant roofing, smart leak detectors, and storm-resistant improvements may also qualify homeowners for additional discounts.

Reviewing your deductible is another option. Choosing a higher deductible usually lowers your monthly premium, although you’ll pay more out of pocket if you file a claim. The best deductible is one that balances affordable premiums with an amount you could comfortably pay during an emergency.

Regular home maintenance can also help control insurance costs. Replacing an aging roof, repairing plumbing issues promptly, updating old electrical wiring, trimming trees near your home, and maintaining heating systems all reduce the likelihood of expensive claims and may improve your home’s insurability.

Perhaps the most important habit is reviewing your homeowners insurance policy every year. As rebuilding costs, home improvements, and insurance options change, your policy should change too. Annual policy reviews help ensure you have the right amount of coverage while taking advantage of any new discounts your insurer may offer.

The reality is that homeowners insurance rates are unlikely to return to the lower levels seen years ago. Rising construction costs, more frequent natural disasters, inflation, and increasing claim expenses continue to shape the insurance market. However, understanding these trends allows homeowners to make informed decisions instead of simply accepting higher premiums without question.

Ultimately, why homeowners insurance rates keep rising in 2026 comes down to one simple idea: the cost of protecting homes has increased. While higher premiums can be frustrating, homeowners who compare quotes regularly, maintain their property, improve home safety, and review their coverage annually are often in the best position to manage costs without compromising the protection their home and family deserve.

Leave a Reply