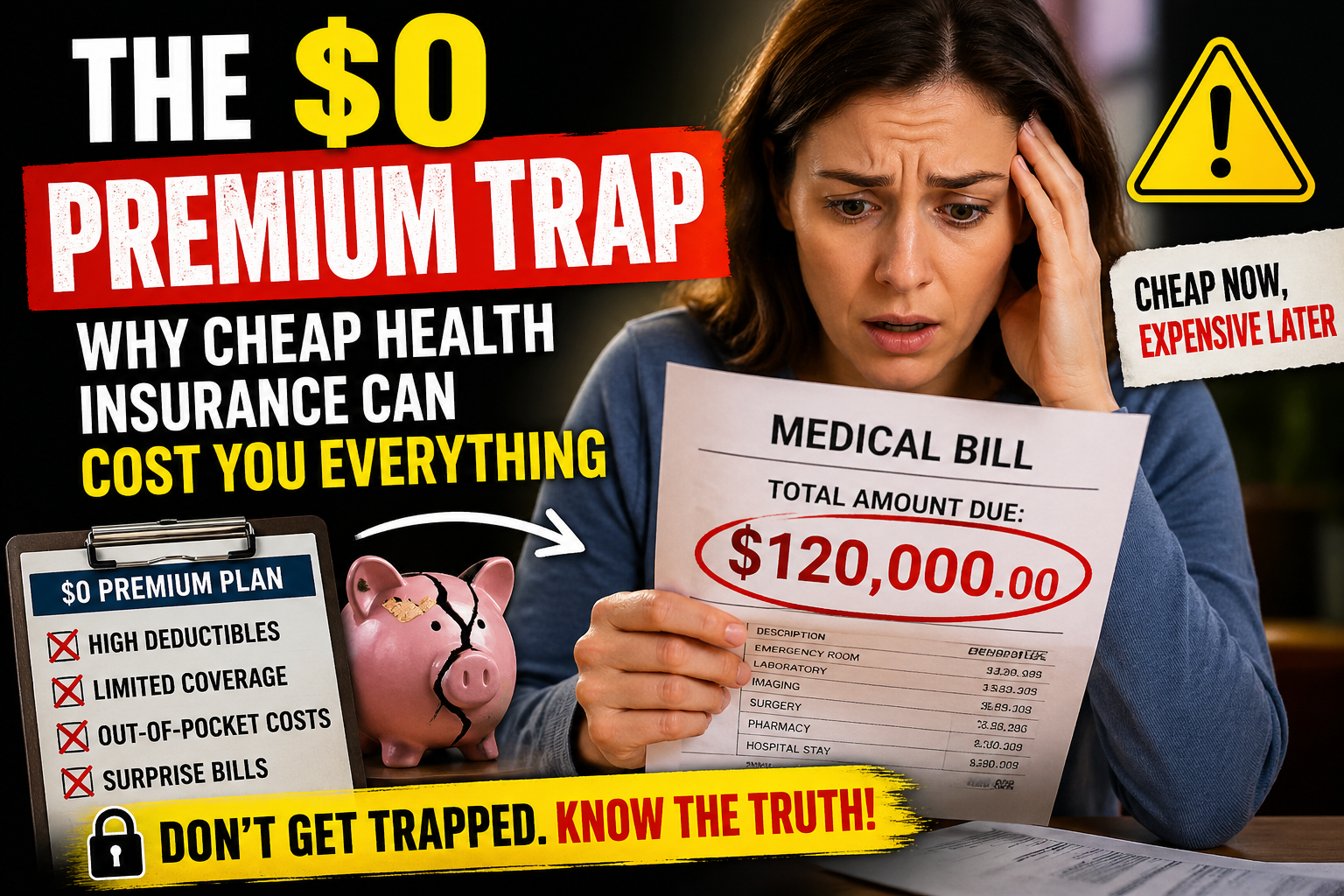

The $0 Premium Trap: Why Cheap Health Insurance Can Cost You Everything

Table of Contents

- The Promise of “Free” Health Insurance

- What a $0 Premium Plan Really Means

- Why Cheap Doesn’t Mean Affordable

- The Hidden Costs Most People Never See

- High Deductibles: The Real Price Tag

- Out-of-Pocket Maximums That Shock You

- Limited Networks: The Access Problem

- Prescription Drug Coverage Gaps

- Emergency Care Isn’t Always Fully Covered

- The Risk of Delayed Care (And Why It Gets Expensive)

- Real Scenario: How a $0 Plan Turns Into Massive Debt

- Who Should Be Careful With $0 Plans

- How to Evaluate a Plan Like an Expert

- Smart Strategies to Avoid the Trap

- Common Mistakes That Cost Thousands

- FAQs

- Conclusion

The Promise of “Free” Health Insurance

A $0 premium health insurance plan sounds like a dream because it removes the monthly burden that many households struggle with, and for millions of Americans browsing marketplace options, it feels like the smartest financial move at first glance; after all, why would anyone willingly pay hundreds of dollars every month if a plan exists that costs nothing upfront, yet promises coverage and protection, but the reality most people discover only after a medical event is that “free” in health insurance is often a marketing illusion rather than true financial safety, and the absence of a monthly premium usually means the cost has simply been shifted into other areas that only become visible when you actually need care, which is exactly when the financial impact hurts the most.

What a $0 Premium Plan Really Means

A $0 premium plan does not mean healthcare is free; it simply means you are not paying a monthly fee to maintain the policy, but every other part of the cost structure—deductibles, copayments, coinsurance, and coverage limitations—still applies, often at higher levels than traditional plans, which means the financial responsibility doesn’t disappear but instead gets delayed until the moment you need medical treatment, and that delay creates a dangerous sense of security because people assume they are protected when, in reality, they are exposed to potentially large out-of-pocket expenses that can quickly add up in real-world situations.

Why Cheap Doesn’t Mean Affordable

True affordability in health insurance is not defined by what you pay each month but by what you pay when something goes wrong, and this is where many people make a critical mistake by choosing the lowest premium without evaluating the total cost of care, because a plan that costs $0 monthly but requires thousands of dollars during an emergency is not truly affordable, especially for families without large savings, and the financial shock of a sudden medical event can turn what seemed like a smart saving decision into a long-term burden that affects stability, debt levels, and overall financial health.

The Hidden Costs Most People Never See

The real danger of $0 premium plans lies in the hidden costs embedded within the policy structure, which often include high deductibles, higher coinsurance rates, limited service coverage, and strict provider networks, and these details are usually buried in lengthy policy documents that most people either skim or completely ignore, assuming the basics are enough to understand the plan, but these overlooked details are exactly what determine how much you will actually pay in a real medical situation, making them far more important than the premium itself.

High Deductibles: The Real Price Tag

High deductibles are one of the most significant features of $0 premium plans, often ranging from several thousand dollars to amounts that can feel overwhelming for the average household, and this means that before your insurance contributes meaningfully to major medical costs, you must first pay that amount out of pocket, which can be financially devastating during emergencies such as surgeries, hospitalizations, or serious illnesses, turning what seemed like a cost-saving plan into a major financial challenge almost overnight.

Out-of-Pocket Maximums That Shock You

While every insurance plan includes an out-of-pocket maximum designed to cap your yearly expenses, these limits can still be extremely high in low-premium plans, often reaching levels that many people are not prepared to handle, and although hitting this maximum technically limits further costs, the journey to reach it can involve significant financial strain, especially when multiple medical services are required in a short period of time, making it essential to understand that this “cap” is not necessarily a safety net for everyone.

Limited Networks: The Access Problem

Another critical issue with $0 premium plans is the restricted network of healthcare providers, which can limit your choices and force you to seek care only from specific doctors and hospitals, and if you unknowingly receive treatment outside this network, your insurance may cover little or none of the cost, which can dramatically increase your financial burden, particularly in urgent situations where you may not have the ability to choose where you receive care.

Prescription Drug Coverage Gaps

Prescription coverage is another area where these plans often fall short, as many include limited formularies that do not fully cover certain medications, especially newer or specialized treatments, which can result in high out-of-pocket costs for individuals who rely on ongoing prescriptions, and this can become a long-term financial issue rather than a one-time expense, particularly for those managing chronic conditions.

Emergency Care Isn’t Always Fully Covered

Although emergency services are generally included in most plans, they are not always covered in a way that eliminates significant personal costs, as follow-up care, specialist consultations, and extended hospital stays may still fall under high deductibles or coinsurance requirements, meaning that even a single emergency can trigger a cascade of expenses that extend far beyond the initial treatment.

The Risk of Delayed Care (And Why It Gets Expensive)

When people know they will have to pay high out-of-pocket costs, they often delay seeking medical care, which can allow minor health issues to develop into more serious and expensive conditions over time, creating a situation where the attempt to save money initially ends up costing significantly more in the long run, both financially and in terms of overall health outcomes.

Real Scenario: How a $0 Plan Turns Into Massive Debt

Consider a situation where someone with a $0 premium plan and a high deductible experiences an unexpected medical emergency, such as an accident requiring hospitalization, and suddenly they are responsible for thousands of dollars before their insurance begins to cover costs, followed by additional expenses through coinsurance, which can quickly accumulate and create a financial burden that feels disproportionate to the idea of having “free” insurance.

Who Should Be Careful With $0 Plans

These plans may work for individuals who rarely use healthcare services, but they can be risky for those with ongoing medical needs, regular prescriptions, or a preference for flexibility in choosing providers, as the limitations and cost structures can create challenges that outweigh the initial savings, making it important to carefully evaluate personal health needs before selecting such a plan.

How to Evaluate a Plan Like an Expert

Instead of focusing solely on the premium, it is essential to evaluate the full structure of the plan, including deductibles, out-of-pocket maximums, provider networks, prescription coverage, and coinsurance rates, because these factors determine the true cost of care and provide a more accurate picture of what you will pay over time.

Smart Strategies to Avoid the Trap

Avoiding the $0 premium trap involves comparing multiple plans, estimating your healthcare needs realistically, choosing balanced coverage even if it comes with a modest premium, and carefully reviewing policy details to ensure you are not exposed to unnecessary financial risk, as a slightly higher monthly cost can often provide significantly better protection when it matters most.

Common Mistakes That Cost Thousands

One of the most common mistakes is choosing a plan based only on its monthly cost without understanding the full financial implications, along with ignoring deductibles, failing to check provider networks, and assuming all services will be covered, all of which can lead to unexpected expenses that far exceed any initial savings.

FAQs

What does a $0 premium health insurance plan actually mean?

It means you do not pay a monthly premium, but you are still responsible for deductibles, copays, and other healthcare costs when you use services.

Is a $0 premium plan really free healthcare?

No, healthcare is not free under these plans; the cost is simply shifted to when you need medical treatment.

Why are deductibles so high in these plans?

Because insurers lower the monthly premium by increasing the amount you must pay out of pocket before coverage begins.

Who should avoid $0 premium plans?

People with chronic conditions, regular medications, or those who expect frequent medical visits should be cautious, as costs can add up quickly.

Can a medical emergency become expensive even with this plan?

Yes, emergencies can lead to thousands of dollars in expenses due to high deductibles and coinsurance requirements.

How can I choose a better plan?

Look beyond the premium and evaluate deductibles, out-of-pocket limits, provider networks, and overall coverage.

Do these plans cover prescription drugs fully?

Not always; many have limited drug coverage, which can result in additional out-of-pocket costs.

Can I switch plans if I realize it’s not suitable?

Usually only during open enrollment or if you qualify for a special enrollment period.

Conclusion

The idea of a $0 premium health insurance plan is appealing, but the reality is far more complex, as the true cost of healthcare is often hidden beneath the surface and only becomes visible when you need it most, making it essential to look beyond the monthly premium and evaluate the full financial picture, because in the world of health insurance, the cheapest option upfront can sometimes become the most expensive decision you ever make.